The implementation the Results based Budget requires a set of norms which, in long term, link the planning, monitoring, evaluation and resources assignment, both within and among them.

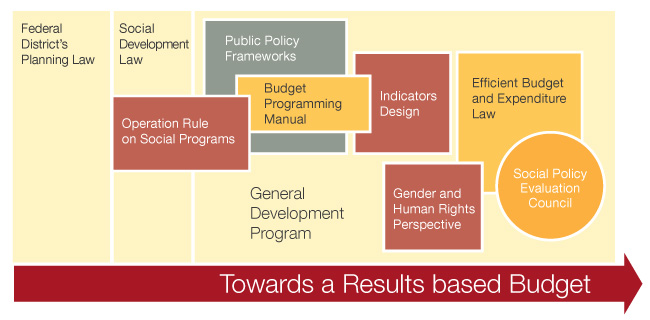

The Planning Act of Mexico City, published in 2000, represented the first step in this connection by requiring that the objectives of the different types of programs defined in it be linked.

However, the Planning Act, doesn’t regulate the more concrete actions of the responsible units that form part of the Mexico city government: i.e. it’s public programs and projects. To take this into account,in 2005, the Social Development Act forced the units responsible of expenditure to define operation rules on social programs. These have to be consistent with the City’s planning, define the way of operating the programs, their beneficiaries, resources and evaluation mechanisms. With these actions, besides maintaining the alignment within the planning system, a way of transitioning to other phases of the BbR is established.

Complementing the operation rules, in 2009 the frameworks of public policy of the responsible units were included in the Program and Budget Manual;instruments through which their actions are linked with the objectives of the General Development Program and other relevant programs for the city’s government. The public policy frameworks also allows foreseeing in which way these actions influence the gender equality and human rights compliance.

Simultaneously to the objectives definition, the regulation framework has required the design of indicators since 2000. Before 2008, the indicators had, mainly, a focus toward processes measurement and goods and services. In this period, the main interest was to have the correct classifications of expenditure (economical and administrative) and administration indicators.

After this year, with the Quarterly Advance Report Guide, it was needed that this design be more focused towards results.The new version of the guide was strengthened in the Efficient Budget and Expenditure Law created in 2010 by including the gender and human rights perspective.

In this last stage, the central government also has issued regulations related to design and monitoring of indicators of the resources it transfers to the federal and municipal entities, as well as the expenditure classifications, accounting issues, and the way of presenting information on Web pages and the rendering of accounts reports, namely public accounts that the federal and municipal governments render to their respective legislatures. The objective of all this is, in a way, that federal governments generate comparable information, a key element when evaluating the pertinence of public policies.

Once the information generation aspects are regulated, the natural question is to know what to do with it. The regulation framework has forced the units responsible of expenditure to make financial evaluations of the investment projects, in order to increase their probability of success. Also, it allows the units to carry out evaluations of any type over any of their projects.

This regulation framework also foresees the commissioning of external evaluations, and in fact, to that effect, the Social Policy Evaluation Council was established in 2008.

The mechanisms responsible for audits also have been regulated, as well as the establishment of committees that survey the compliance of certain policies. Actually, civil organizations participation in these committees has stood out.

The regulation changes have, undoubtedly been useful to redefine strategies, optimize and assign resources, always considering the economic, transparency, efficacy, efficiency and budget balance principles.